The distinctive tale of the UK economy in May 2026

UK bond yields are at their peak at 2008 levels with UK 30-year bond yield reaching 5.81% on 18 May 2026. UK government debt is as high as once seen in the 1960s post the second world war. UK’s political environment hasn’t been more chaotic than today with Starmer’s seat weakening day by day. The number of takeovers in the UK is at record high (up 250% in 2026 with inbound M&A value at their highest in more than a decade) whereas listings are at record lows. These trends compel us to dive deeper into what is driving the economy today and what it is means for business.

Economic snapshot on 18 May 2026

UK at the moment is in a very chaotic space. While the bond yields are rising (i.e. investors are seeking a higher premium as risk is increasing due to multiple factors adding complexity), the total debt is also at its peak indicating there is still the need and demand. To back it up with numbers:

- The 30-year gilt yield reached 5.81% on 18 May 2026, a level not seen since 1998.

- The 10-year gilt yield is around 5.2%, the highest since 2008 (rising c.35 basis points over the last month).

- UK public sector debt is at 93.8% of the GDP as of end of March 2026, a ratio not seen since 1960s (post World War II).

- The Office for Budget Responsibility downgraded UK’s growth forecast to 1.1% for 2026 with potential mid-term output stuck around 1.5%, the same dynamic as observed around 2010.

- RPI inflation is around 3.1%, well above the target.

- The Debt Management Office syndicated £15bn of new 2036 gilt in April at 4.92% while it drew a record £148bn of investor orders (according to Bloomberg).

From the stats it is clear that the market is requiring a higher premium to lend to the UK. This is an example of a nation with weak output but mounting liabilities. The crux of the issue is not just the numbers. These numbers are purely a result of what is happening underneath i.e. uncertainties around the impact of the US-Iran war as well as no clear direction of the political environment.

Keir Starmer’s position is steadily weakening since the start of this month and main opposition is coming from within Labour itself. Bloomberg’s market commentary directly attributes an extent of the yield surge to domestic political uncertainty layered on top of international energy and inflation pressures. The combination of fiscal credibility questions, an uncertain succession and BoE’s struggle in keeping inflation at bay has resulted in a premium that is higher than it was for a long time.

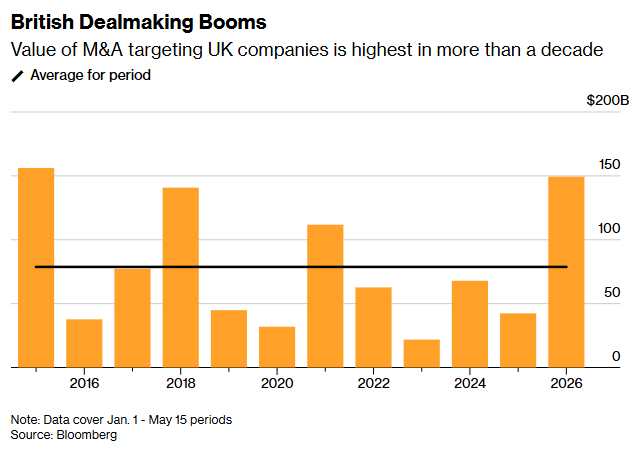

While gilts are pricing in a higher risk, M&A market is on a buying spree. The value of takeovers targeting UK businesses is up 250% this year reaching c.$150bn according to data compiled by Bloomberg, positioning UK M&A advisors for their best year in almost a decade. In particular, international acquirers are treating UK assets as compelling value assets since the businesses listed on the LSE have often been regarded as “gold standard” due to high scrutiny and reporting / governance requirements historically.

Some of the notable UK businesses which have agreed tie ups with overseas competitors include Unilever and Schroders.

The crux of the issue

One of the key drivers of growth in any economy is the investment businesses make to drive revenue which eventually drives growth. Yes we are talking about capex. According to ONS, UK business investment increased 0.7% in Q1 this year. While this is a growth, it is still 1.8% lower than Q1 2025. Slowing capex translates into productivity stagnation leading to slower growth compared to the rise in debt, which eventually leads to a sell in debt and that leads to international buyers flooding in to buy assets for cheap. It is a loop. UK was already grappling with this issue due to Ukraine war, US-Iran war, inflation, etc. To add to this, domestic political uncertainty means the path is not going to be straightforward. Depending on which political party comes to force and what their manifesto aims for, will decide whether the government takes a more expansionary or restrictive fiscal stance, which will in turn influence inflation, jobs, capex decisions and M&A activity. That will also decide the BoE rates which then impacts debt and the loop continues. Yes it is as confusing and chaotic as it sounds above, read it multiple times!

What is truly needed in this country?

It seems the country needs clarity on the below three issues:

Stability in the cost of doing business

Narrow margins topped by increasing employer NIC, frozen tax thresholds and increase in wages have strained earnings. With inflation and rate uncertainty, the margins remain strained. It is crucial to give businesses clarity around these costs in order to avoid mass firing, withholding of capex and overall cautious sentiment. However, the answer is not straightforward.

Clarity in capital allowances

While full expensing has been helpful, a cut down of writing-down allowance to 14% from 2026 will impact capital intensive businesses.

Transformation in listings and institutional capital regulation

The FCA’s pro-growth listings reforms are just the start. Sustaining IPO momentum requires a steer to keep favouring growth and structurally encouraging UK pensions and institutional investors to back domestic listings. UK’s £1.3trn pension pool is currently being fought over in London. The actual question is, how to channel this money back into the UK economy to encourage growth.

Final thoughts

The country is in a very interesting position today. Gilt markets and international buyers are simply taking advantages on the structural weaknesses. The country has the capital, talent, institutional depth and regulatory infrastructure. All it needs is policy stability and lifting the fog on long-term trajectory which comes from domestic as well as international geopolitical stability and/or clarity of direction. The way out is steady, sustained implementation of modern, reliable frameworks that are built for the fast-growing and evolving future. From the market sentiment it is clear that UK understands it cannot simply assume a dominant position in international business and is already bracing to demonstrate its key differentiator i.e. quality and sustainability of its assets. How it unfolds and by when is a matter of time.

Views expressed are the author's own and do not represent any employer or constitute any investment advice.

Ria Vaghela

MSc Finance graduate from the London School of Economics and Political Science (LSE)

Ria V Vaghela is an M&A Associate at RSM UK and an MSc Finance graduate from the London School of Economics and Political Science (LSE). She has worked at Jefferies, Dial Partners, GP Bullhound and 7i Capital prior to RSM UK gaining an extensive experience in finance. She has also worked as an Editor and Content Writer for The Representative Media. Apart from finance, she is interested in reading books on philosophy, self-help and economics, likes to paint and play lawn tennis.

Recommended Posts

From AI Hype to AI Proof

July 18, 2026

What Private Markets Taught Me About Long-Term Thinking

July 16, 2026