Scam 2026!

News platforms are buzzing with the Rs. 15 lakh crore Rajesh Exports misrepresentation uncovered by SEBI last week. Yes, the title was clickbait as this case isn’t officially a scam since SEBI is still investigating the case! But the story sounds no less than one. Since you already know the basics, let’s not dwell on the facts and focus on the interesting bits.

For those who aren’t aware…

Rajesh Exports is a Bangalore, India-based gold and diamond jewellery business offering services across the entire value chain from mining to export and retail sales. Although the business was run as a small family jewellery business, in 1994, just 6 years since the two brothers joined the business, Rajesh Exports became India’s largest exporter and wholesaler of gold jewellery. In 1995, it listed its securities on the BSE and NSE to expand a manufacturing facility. The journey since was simply upwards – expansion after expansion. Between 2015 and 2016, its sales grew from $8bn to $24bn, in ONE YEAR! Of course the business was in the limelight with its massive growth but considering the safe space it was in, nobody would have thought what would come next.

According to a handful of sources such as the Economic Times, Moneycontrol and Firstpost, one of the shareholders of Rajesh Exports in March 2024 reported to SEBI that something was not right about the business’ books with huge amounts of trade receivables sitting on the balance sheet for 2+ years. This triggered SEBI to investigate the books. After 2 years on 3rd June 2026, SEBI issued an interim order claiming that Rajesh Exports has many discrepancies in its financial reports from FY21 to FY25. It claims that the business has reported far more revenue than it actually generated showing a discrepancy of almost Rs. 15 lakh crores. Following these claims and non-cooperation with the inquiry, SEBI has also disallowed Mr. Rajesh Mehta from dealing in securities and is keen that the business rectifies its books. It is anticipated that 97-99% of revenue that came from overseas was completely misrepresented potentially claiming the full value of gold as revenue rather than just the commissions but of course this is all anticipation and not a proven fact yet. The worry is that investors will lose crores if this company is truly in a deep hole that SEBI is claiming. For example, LIC has a 10.8% stake of the business which means large institutions will also lose money and the trickle-down effect in this market will be worse.

But here’s the interesting part…

One did not need SEBI to highlight the issues. Recall the jump in revenue I mentioned earlier? In 2015, Rajesh Exports acquired Valcambi, the world’s largest gold refinery. This Swiss company is at the heart of this entire scam. The 97-99% revenue that SEBI is claiming, most of it seems to be linked to Valcambi. But Valcambi’s own accounts, audited by KPMG in Switzerland, show revenue of about Rs. 543 crore. That’s less than half a percent of what the group above it reported.

SEBI’s question is a simple one. If Valcambi is the business actually doing the work, why does it report Rs. 543 crore, while the holding company sitting on top of it, which by SEBI’s account does nothing day-to-day, reports nearly Rs. 3 lakh crore?

The company’s answer is that Valcambi only books its processing fee, while another group entity books the full value of the gold. SEBI isn’t convinced, and says the numbers don’t hold together and can’t be backed by records it can actually check.

This is the bit worth holding onto. Gold trading runs on wafer-thin margins, a few rupees for handling metal worth lakhs. So the real question is whether the company counted the gross value of the gold as its revenue, or just the thin slice it actually earned. Count the gross, and a modest operation looks enormous overnight. SEBI’s case goes further still, that a chunk of these entries weren’t real trade at all but were tied to Rajesh Mehta’s personal derivative positions, inflating turnover with nothing real underneath. The order also points to money moving into Mehta’s personal accounts, and puts investor losses so far at around Rs. 12,726 crore.

To be clear, none of this is settled. SEBI’s order is an early, one-sided view, the company says its revenues are correct and that there’s simply been confusion with the regulator, and the forensic audit is still running.

…and it was never quite hidden!

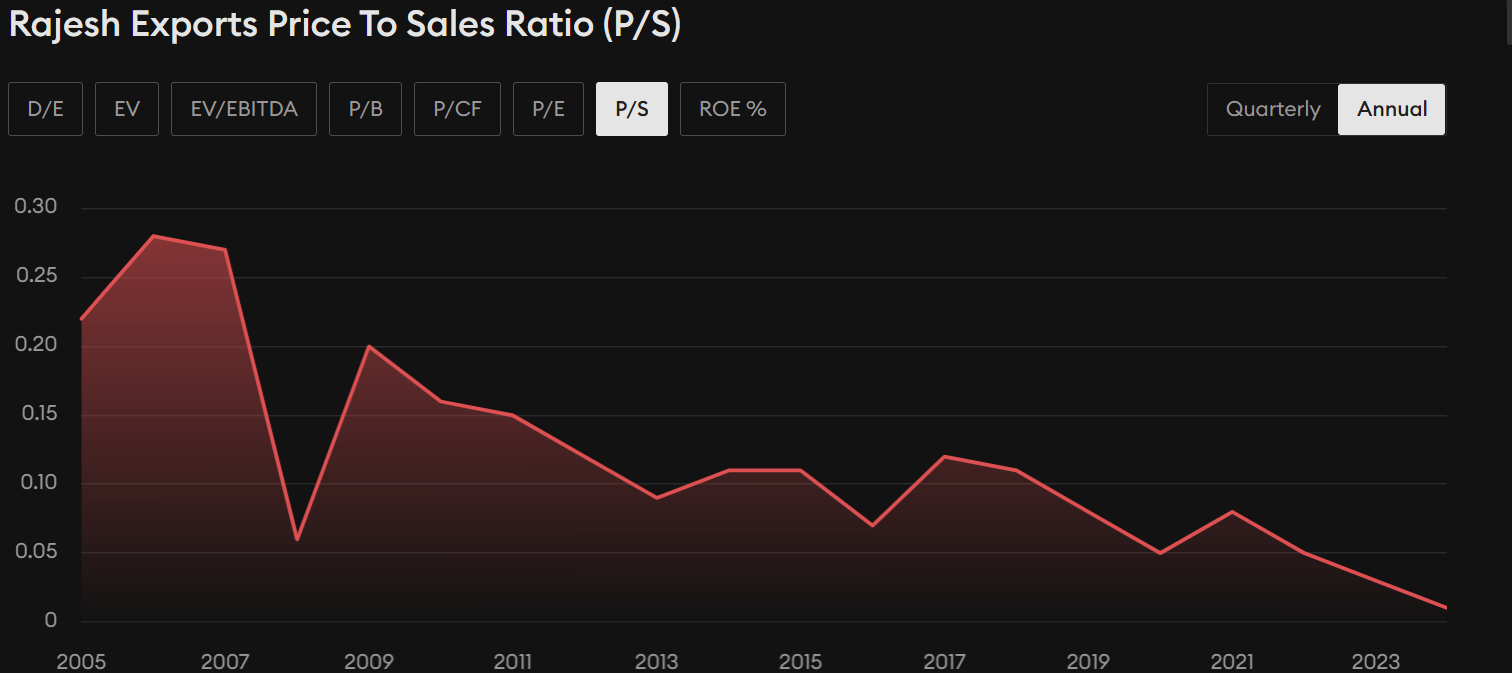

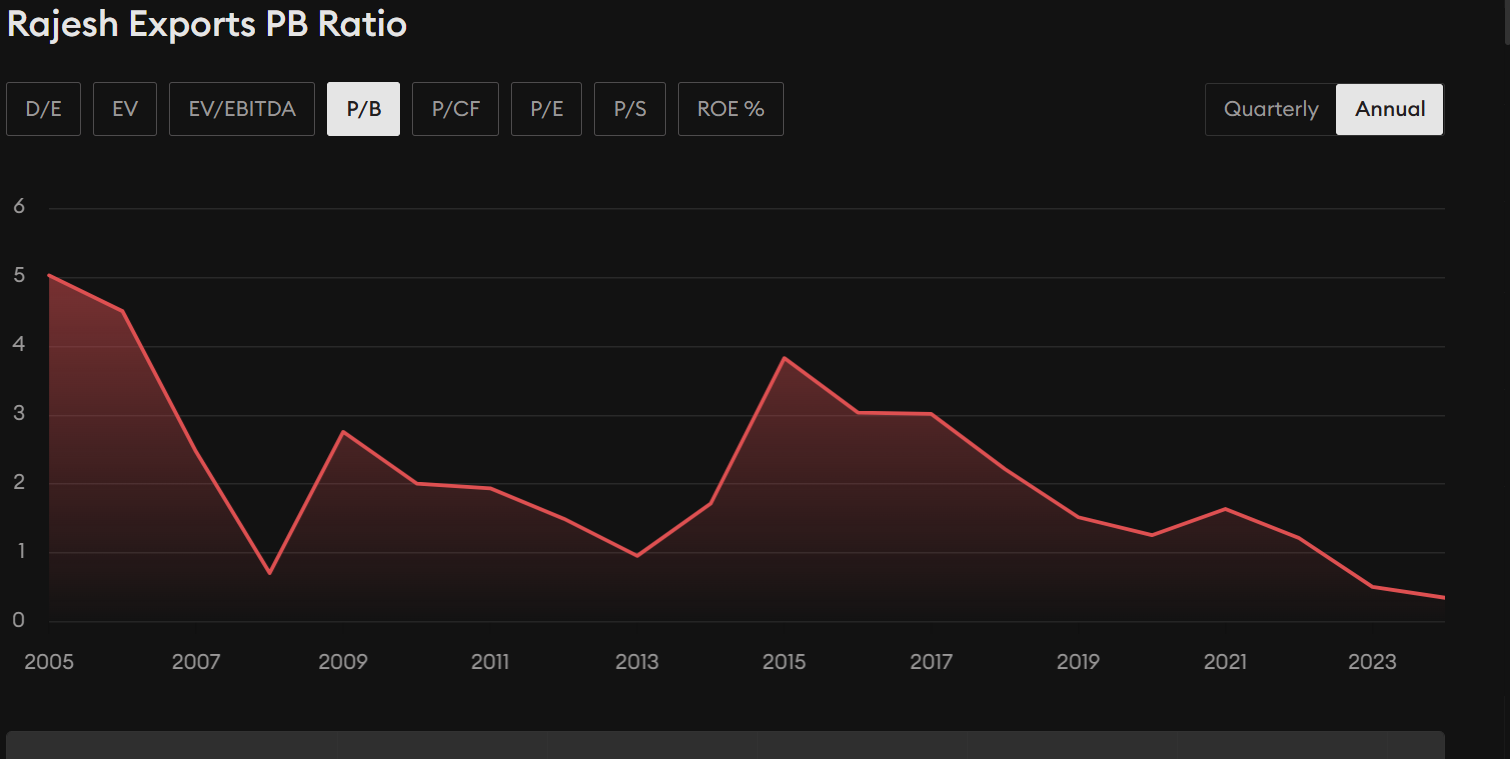

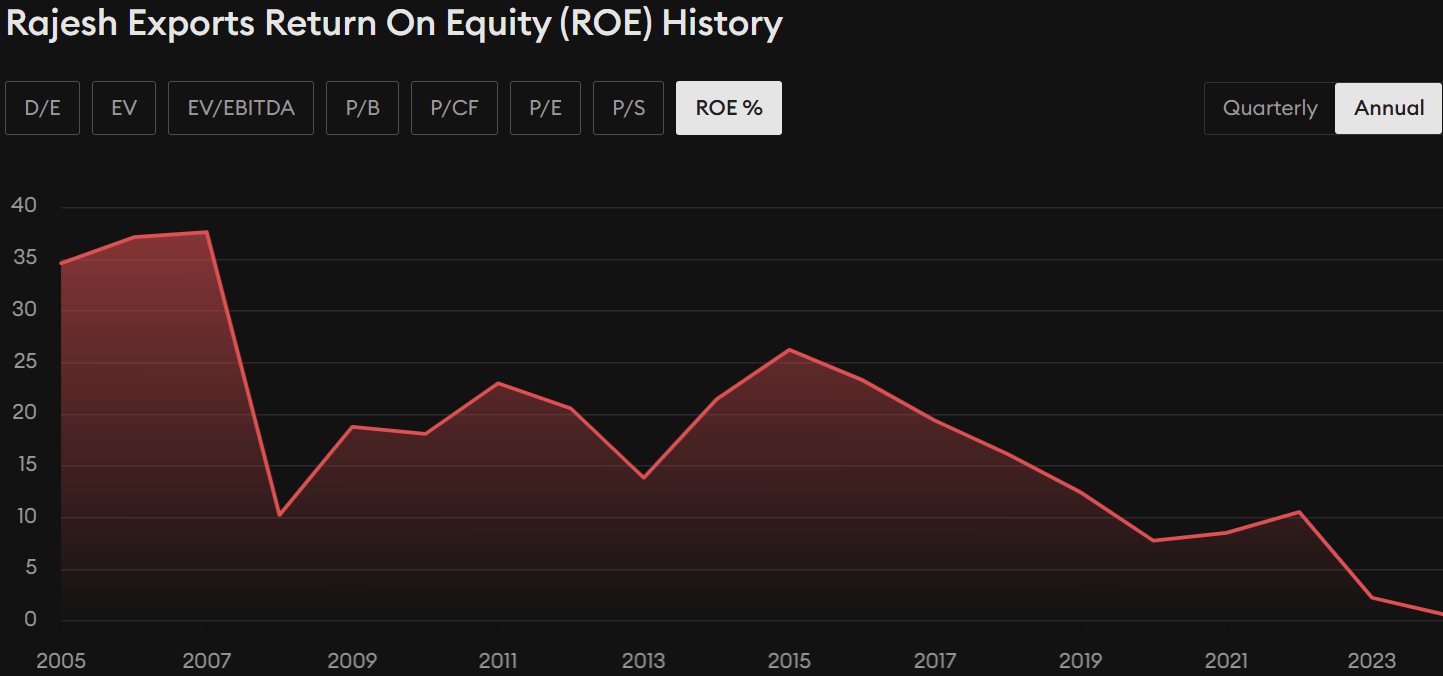

If you see the price to sales ratio of the business in the chart below, you can see that it was always obvious with a declining trend with ROE and price to book ratio too falling since 2015.

This shows how easy it is for us to get lost in the revenue story and completely ignore the core fundamentals. It also shows the importance of zooming out once in a while to understand the true picture underneath the branding.

Parting thoughts!

This story reveals how one shareholder voice can help uncover scams, but also reveals how important it is to be flexible as an investor to look at multiple indicators, multiple time frames and question every number and story sold.

Regardless, I’ll be watching how this one plays out.

Disclaimer: The views expressed here are my own and do not represent those of my employer. This is general commentary on a developing, publicly reported matter, and nothing here is investment advice. The findings described are SEBI's, from an interim order; the company denies wrongdoing and the matter remains under investigation.

Ria Vaghela

MSc Finance graduate from the London School of Economics and Political Science (LSE)

Ria V Vaghela is an M&A Associate at RSM UK and an MSc Finance graduate from the London School of Economics and Political Science (LSE). She has worked at Jefferies, Dial Partners, GP Bullhound and 7i Capital prior to RSM UK gaining an extensive experience in finance. She has also worked as an Editor and Content Writer for The Representative Media. Apart from finance, she is interested in reading books on philosophy, self-help and economics, likes to paint and play lawn tennis.

Recommended Posts

From AI Hype to AI Proof

July 18, 2026

What Private Markets Taught Me About Long-Term Thinking

July 16, 2026