Event Driven Investing Explained: Hedge Funds, Merger Arbitrage and the Paramount WBD Deal

Hedge funds, arbitrage and hedging are some of the most interesting terms in finance. They are also among the most misunderstood.

When many people hear the phrase hedge fund, they imagine complex algorithms, high frequency trading and traders sitting in front of several screens trying to beat the market.

However, after spending time reading about different hedge fund strategies, it becomes clear that many of these strategies are built on fairly intuitive ideas.

One strategy that I have personally found particularly interesting is event driven investing.

Before going further, a quick note on context. I work in mergers and acquisitions, but I do not work in hedge funds or asset management. The goal of this article is simply to explain what I have learned about event driven strategies and merger arbitrage, using a real example from the media industry, the proposed Paramount acquisition of Warner Bros. Discovery.

What Do Hedge Funds Actually Try to Do?

Most hedge funds aim to generate something known as alpha. In simple terms, alpha refers to returns that cannot be explained purely by overall market movements. For example, if the stock market rises by 10% and a portfolio also rises by 10%, the portfolio has simply moved with the market. However, if the portfolio rises by 15% when the market rises by 10%, the additional return may be considered alpha.

Classic finance textbooks such as Investments by Bodie, Kane and Marcus describe alpha as the part of a portfolio’s return that comes from strategy or insight, rather than simply being exposed to the market.

Different hedge funds attempt to generate alpha in different ways. Some focus on long short equity strategies, others trade macroeconomic trends, while some rely heavily on quantitative models.

Another large category is event driven investing, which focuses on corporate events that may change the value of a company.

What Is Event Driven Investing?

Event driven investing focuses on situations where a significant corporate event is taking place.

Examples include:

- mergers and acquisitions

- corporate restructurings

- spin offs

- bankruptcies

These events often create uncertainty. When uncertainty increases, markets sometimes struggle to price assets perfectly in the short term. Investors who specialise in event driven strategies analyse these situations and attempt to take positions based on the probability of different outcomes. One of the most well known strategies in this space is merger arbitrage.

Understanding Merger Arbitrage

When a company announces that it plans to acquire another company, the target company’s share price usually jumps.

However, the price almost never rises fully to the offer price immediately.

For example, if a company announces that it will acquire another firm for $31 per share, the target company might trade at $28 or $29 instead. The difference between the offer price and the market price is known as the merger spread. This spread exists because markets understand that not all deals actually close.

Several things could cause a deal to fail:

- regulators might block the transaction

- financing might fall apart

- shareholders might reject the proposal

- market conditions might change

Merger arbitrage investors attempt to capture this spread by buying the target company’s shares while assessing the risk that the deal might not go through.

The Paramount Warner Bros Discovery Situation

A useful example of this strategy can be seen in the proposed Paramount Skydance acquisition of Warner Bros Discovery. In February 2026, Paramount Skydance reached an agreement to acquire Warner Bros Discovery for $31 per share, valuing the company at roughly:

- $80bn in equity value

- c.$110bn in enterprise value

The transaction is expected to generate approximately $6bn in synergies and is targeted to close in the Q3 2026.

From a strategic perspective, the rationale appears to be scale. If completed, the combined company would control a very large content library, including more than 15,000 film titles and thousands of hours of television programming. The company would also have stronger sports broadcasting rights and a larger direct to consumer streaming platform. In an increasingly competitive streaming industry, scale and content ownership have become important advantages.

Financing the Deal

The financing structure behind the transaction is also significant.

Approximately $47bn is expected to come from equity investments, including funding from:

- the Ellison family

- RedBird Capital

Another $54bn is expected to be financed through debt arranged by banks such as:

- Bank of America

- Citigroup

- Apollo

At one stage the situation became even more interesting when Netflix reportedly explored a competing bid, briefly raising the possibility of a bidding battle before eventually stepping away. Situations like this are exactly the type that event driven investors monitor closely.

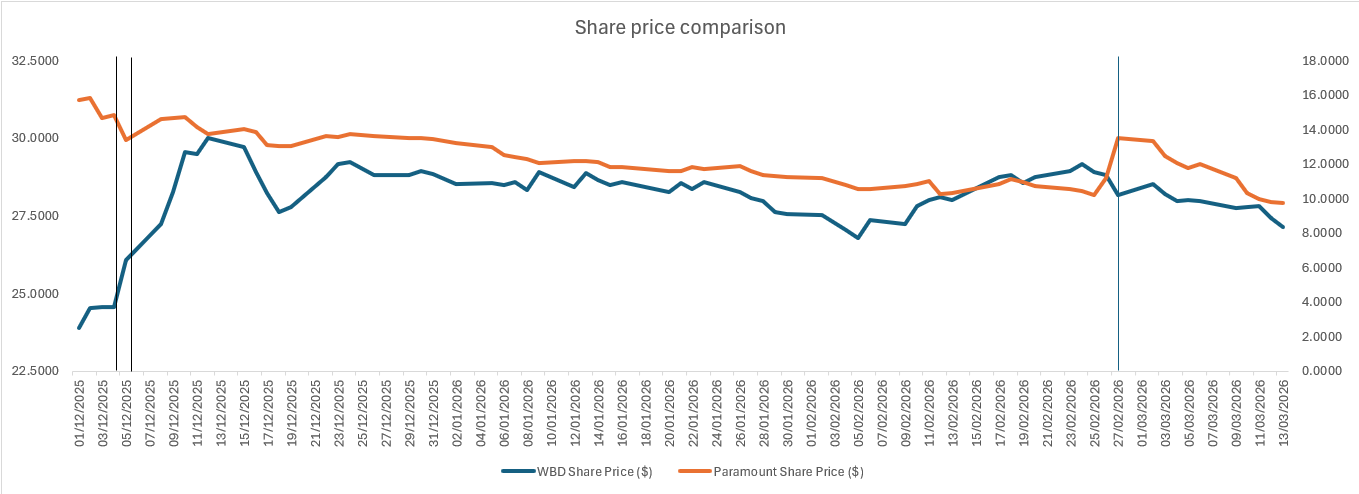

How the Market Reacted

One of the most interesting aspects of this situation is how stock prices reacted as new information emerged.

When Paramount first submitted its bid, Warner Bros Discovery’s share price increased, reflecting the takeover premium being offered. At the same time, Paramount’s share price declined, likely because investors were concerned about financing risk and execution challenges.

Later, when Netflix appeared as a potential competing bidder, WBD’s share price rose further as the market started pricing in the possibility of a higher offer. Paramount’s share price also stabilised as investors reassessed the strategic implications of the deal.

Eventually, as the market began anticipating that Paramount would ultimately secure the acquisition, both companies’ share prices started adjusting again even before any final confirmation.

Event study

The chart captures three moments that shaped market expectations:

- Paramount submitting the initial bid

- Netflix entering the bidding process

- Paramount ultimately securing the deal

Looking at the price movements around these points gives a good sense of how markets gradually update their expectations about whether a deal will actually happen.

The Merger Spread

On 4 December 2025, Warner Bros. Discovery was trading at $24.54, which implied a merger spread of roughly 26.3% relative to the eventual $31 offer price. By 27 February 2026, the share price had moved to $28.17, narrowing the spread to about 10%.

A narrowing spread usually suggests that the market is becoming more confident that the deal will go through. At the same time, the spread rarely disappears completely until the deal actually closes because there are always risks involved.

What Could Still Go Wrong?

Two risks stand out in this case.

Regulatory approval

Large media mergers often attract scrutiny from competition authorities, particularly when they involve streaming platforms, film production and sports broadcasting rights.

Financing risk

Paramount’s debt has reportedly been downgraded to junk status, which could make the debt portion of the financing package more expensive or difficult to secure.

If the deal were to collapse, Warner Bros Discovery’s share price could fall back toward pre announcement levels since much of its recent price movement reflects the merger premium. Paramount’s share price could also decline if the expected synergies fail to materialise.

Final thoughts

One reason event driven investing is so interesting is that it focuses on specific corporate situations rather than broad market predictions. Instead of trying to predict where markets will go, investors analyse events, probabilities and deal structures.

The Paramount Warner Bros Discovery situation is still unfolding, but it provides a useful example of how markets react to corporate events and how the merger spread evolves as the probability of completion changes.

For anyone interested in markets and corporate finance, situations like these provide a useful window into how professional investors analyse deals.

Disclaimer: This article is written purely for educational and informational purposes. It reflects my personal understanding and analysis of publicly available information. Nothing in this article should be interpreted as financial or investment advice. Investing involves risk. Readers should conduct their own research or consult a qualified financial professional before making any investment decisions.

Ria Vaghela

MSc Finance graduate from the London School of Economics and Political Science (LSE)

Ria V Vaghela is an M&A Associate at RSM UK and an MSc Finance graduate from the London School of Economics and Political Science (LSE). She has worked at Jefferies, Dial Partners, GP Bullhound and 7i Capital prior to RSM UK gaining an extensive experience in finance. She has also worked as an Editor and Content Writer for The Representative Media. Apart from finance, she is interested in reading books on philosophy, self-help and economics, likes to paint and play lawn tennis.

Recommended Posts

Scam 2026!

June 7, 2026

The distinctive tale of the UK economy in May 2026

May 19, 2026

Understanding politics from a financial lens

May 12, 2026